It was never supposed to be like this #4/50

It was never supposed to be like this #4/50

The worst gas fee ever, why Venmo is free, & the power of (NFT) community

The single worst crypto transaction happened this week.

It represents everything going wrong with cryptocurrencies but everything right about NFTs.

Let me show it to you:

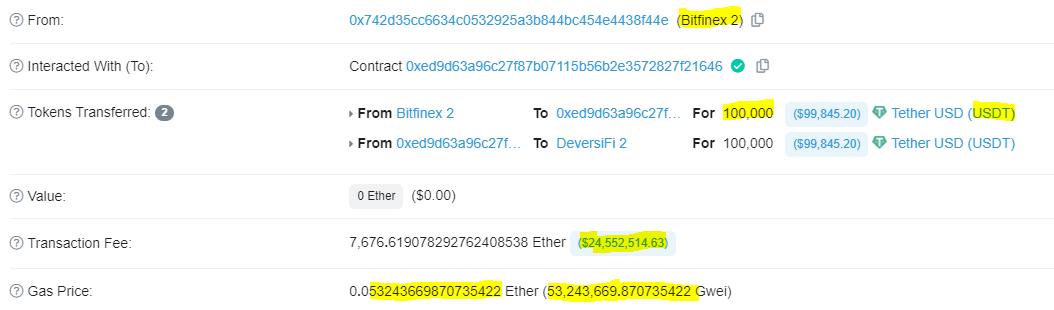

A user was transferring 100,000 USDT from a hardware wallet to DeversiFi — that’s $100,000 USD in Tether, a coin pegged to the US Dollar.

Effectively, this was a bank transfer from one account to another, in the same currency, owned by the same person. A typical wire transfer between bank accounts is somewhere between free to a few dollars.

The gas price was 0.053 Ether — so the transaction should have cost $153.70, which admittedly is high.

Instead, it cost $24,552,514.

That’s right, this $100k transfer cost $24.5m.

Friction & Fees

Cryptocurrency’s original promise was that it could eliminate friction from the financial system.

A company like Visa creates trusts between two people who don’t know each other but want to exchange money. That trust comes at a cost to the consumer, through credit card interest rates, and to the merchant, in the form of a transaction fee.

In 2008, when Satoshi Nakamoto authored the peer-to-peer cryptocurrency paper that spawned Bitcoin, a typical credit card transaction cost 3% to the merchant and required special point of sale hardware tools.

These POS systems were not easy to use, required extensive training, and could be very unreliable. (In other words, they could be real POSes.)

Point of Sale (POS) system, circa 2008

This period in the United States was also marked by financial market failures and the inability of the government to successfully regulate those issues. The 2008 financial crisis drove a sub-movement of deep distrust of the government-backed banking system – this is when the sarcastic term “fiat currencies” first appeared as a way of denouncing faith-based economic systems, like the US who had long since left the gold standard.

A critique of the modern financial system was that it was based on secrecy - two people who wanted to transact needed a trusted third party whose influence and oversight perhaps was unwanted - and this secrecy turned out to have dire economic consequences as banks took egregious risks in the housing market.

The systems entrusted with financial stability nearly brought down their own financial systems.

So why do we need them, anyway?

New Privacy Models

Banks and credit card companies act like referees, making sure transactions are fair and legal. But like referees, there is a cost: the coordination required overhead for fraud protection, identity verification, and absorbing the risk that the buyer or the merchant wouldn’t follow through on their commitments.

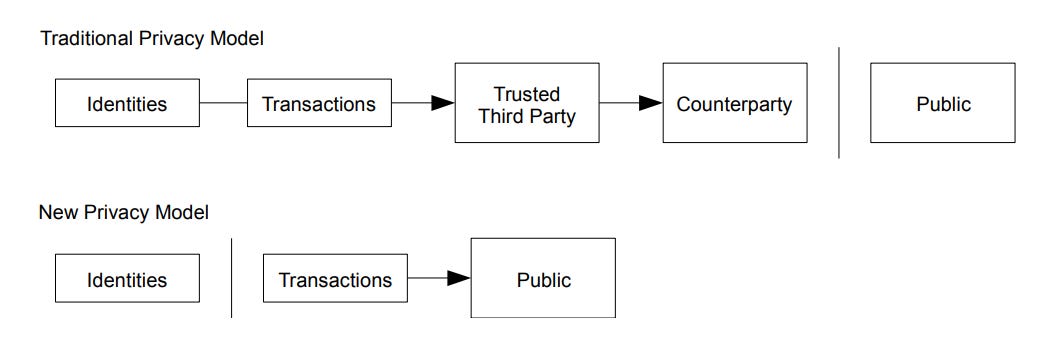

Nakamoto summarized this as the “traditional privacy model”:

From Nakamoto’s Bitcoin Working Paper, Nov 1, 2008

A functional peer-to-peer system inverts that process. What if, instead of paying a referee, both sides agreed to preset rules and just played fair?

Nakomoto’s “New Privacy Model” inverts the traditional model, so identities are unknown but all transactions are public. (This public ledger is how, for example, I can drop in and see the $24.5m transaction above — anyone can, just follow the transfers.)

If every transaction is instantly available and digitally signed, the theoretical risk of fraud is zero since both parties “know” they are entering into a valid contract at the same time.

This should also mean the costs of the traditional privacy model — all that overhead, reporting, risk management, hardware, insipid brand advertising (Visa, it’s everywhere you want to be) — can be eliminated as the source of verifying transactions is left up to the players and the referee is no longer needed.

Get rid of all that infrastructure with peer-to-peer transactions and the fees should be close to zero.

Except, right now, crypto fees are somewhere between $150 and $24.5 million dollars.

And for fiat? Often free.

The Killer P2P App: the Mobile Phone

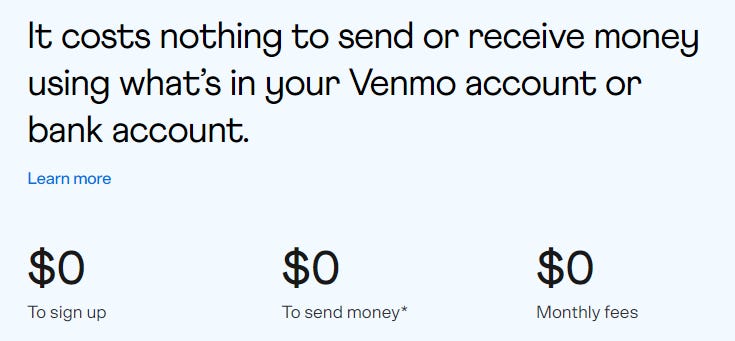

Venmo started in 2010 when college friends Andrew Kortina and Iqram Magdon-Ismail saw first-hand how bad POS systems were, helping a friend with their yogurt shop, in contrast to how simple it could be with a mobile phone.

A mobile phone, as an agent of a transaction, is ingenious: phone numbers are uniquely identifiable, can permit encrypted transactions, and provide digital signatures. In short, they’re a killer app for peer-to-peer payments.

It’s also why Venmo is free - the system has largely been de-risked within the traditional finance ecosystem.

In contrast, transaction costs in cryptocurrency are largely a function of incentives for miners to secure the entire network (Bitcoin) or specific contracts (Ether). What cyrpto has done is moved the infrastructure costs from a centralized system (like Visa) to a plurality of decentralized options.

The benefits of centralization is that there is a single throat to choke when something goes wrong.

Always Blame the JavaScript

Decentralization invites chaos.

More moving parts means more things that can go wrong.

And what happened with the $24.5m transaction is not that someone fat-fingered a key.

There were two technical things which I’ll try and summarize as best I can:

DeversiFi’s JS code that entered the transaction contained a conflict with the two max gas fees settings that safely allow users to set a priority for a transaction (excellent technical deep dive here: https://blog.deversifi.com/23-7-million-dollar-ethereum-transaction-fee-post-mortem/)

The hardware wallet (Ledger) displayed the ETH gas fee as a hexadecimal since the fee was so unexpectedly and absurdly high, an alert the user presumably missed

Ledger hardware wallet, displaying max gas fees as a hex not a financial cost

As ETH gas fees are a bidding function, if someone bids high enough, their transaction gets bumped up. This is why if you’ve ever tried to send an ETH transaction, you’ll notice gas fees vary greatly depending on how much traffic is on the network.

A $24.5m bounty went straight to the top of the list, the transaction happened in less than a minute, and the ETH left the user’s wallet, just as the system is supposed to work.

Except - that transaction was crazy!

Visa would never have let that happen!

They would have called up their customer and said, “something looks really wrong with this transfer” and the story ends there.

Technically, nothing went wrong since the account had enough ETH to cover the fee — with a smaller account, the transaction would have just failed.

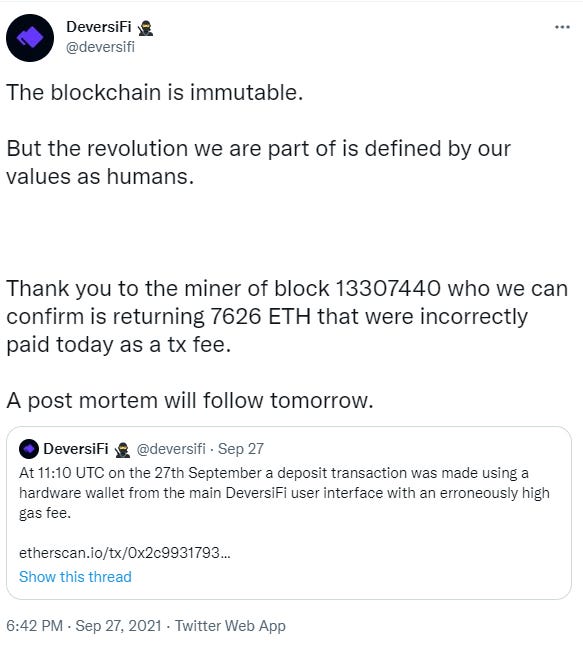

A miner won the lottery, collecting $24.5m for a single transaction.

Until he gave it back.

The Power of Community

Since the blockchain is public, the identity of the miner was quickly uncovered and Deversifi reached out, explaining the situation.

And the miner returned the fee, collecting 50 ETH (~$150k) for his trouble.

Just to be clear - the miner did not need to return the fee. There was nothing that DeversiFi could do to compel the fee to be returned. There was no centralized authority to call to overturn the transaction; it was minted.

The reason the community is so critical to this grand experiment of cryptocurrency, NFTs, and alternative assets is that the community itself becomes a system of creating trust. This miner was a Top 10 miner, well known in the community.

If you know the reputation of who you’re transacting with, that can reduce the amount of risk and potential cost dramatically. Conversely, if you’ve every been in a Discord and been hit up by your new bot friend pumping Sleepy Vampire Babies*, you know how valuable a centralized system can be. (Srsly, guys stop.)

In NFT communities, trust is established through consistent investment, visibility, and advocacy of a project. NFT communities likewise need managers to ensure the viability and safety of the participants. Trust flows differently and it’s not tied up just in the token.

We’ve had these systems before. They’re not banks, they’re governments.

I’ve begun to wonder if I’ve been thinking about NFTs all wrong.

Next time (probably):

What if NFTs are new forms of government?

The perils of brand success

What French Wines can teach us about NFTs

The coming waves of NFT thefts

Tweet of the Moment

Relief is palpable:

I know, I didn’t even touch on what I wanted to write about last week.

As always, I have so much more to tell you,

Paul

P.S. * I don’t think Sleepy Vampires Babies is a project, but my public wallet is paulgriffiths.eth and send me the alien/zombie variant, thanks

=-=-=-=-=-=-=-=-=-=-=

References: